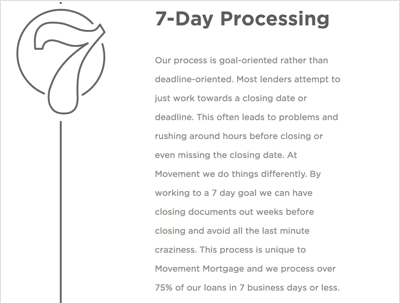

Movement Mortgage’s claim to fame is processing the majority of home loans in seven business days or less. The firm underwrites loans at the beginning of the process in roughly six hours or less, helping speed up the entire loan process from start to finish.

The non-bank mortgage lender was founded in 2008 by Toby Harris, a former vice president at National City Mortgage, and former Super Bowl champion, Casey Crawford. In the past decade, Movement Mortgage has served over 59,000 customers and has grown to 4,500 employees. The company is headquartered in Fort Mill, South Carolina and has 775 locations and can service loans in all 50 states. Montana is the only state the company does not originate loans in.

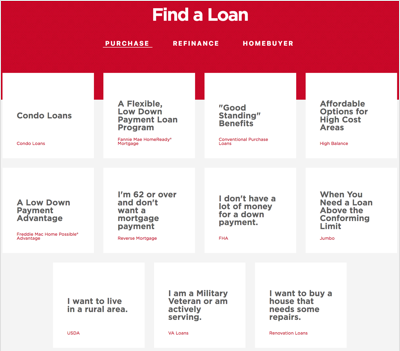

Movement Mortgage offers conventional loans as well as government-backed options such as VA, USDA and FHA loans.

Today's Rates

| Product | Today | Last Week | Change |

|---|---|---|---|

| 30 year fixed | 5.75% | 5.88% | -0.13 |

| 15 year fixed | 5.25% | 5.44% | -0.19 |

| 5/1 ARM | 6.06% | 6.06% | 0.00 |

| 30 yr fixed mtg refi | 7.21% | 7.13% | +0.08 |

| 15 yr fixed mtg refi | 6.59% | 6.73% | -0.14 |

| 7/1 ARM refi | 6.13% | 6.13% | 0.00 |

| 15 yr jumbo fixed mtg refi | 3.06% | 3.10% | -0.04 |

National Mortgage Rates

Regions Served by Movement Mortgage

Does Movement Mortgage Operate in My Area?

Movement Mortgage has 515 offices in 49 states. The company is licensed in every state except Montana.

What Kind of Mortgage Can I Get With Movement Mortgage?

Conventional: This is the standard mortgage loan. You need a 20% down payment to avoid paying private mortgage insurance and a decent credit score to qualify for a conventional mortgage. This type of loan does not have property restrictions, a downside of many government-backed loans. Movement offers conventional fixed-rate and adjustable-rate mortgages.

Jumbo loan: If you’re looking to buy a home in an expensive housing market, you may need to opt for this type of loan. Jumbo loans are loans above the conforming limits set by Fannie Mae and Freddie Mac, two government-sponsored home loan entities. The limit in most areas is $726,200. These type of loans generally require 20% down.

Veterans Affairs (VA) loan: Aimed at veterans, service members, National Guard and Reserve personnel, VA loans offer homeownership opportunities under favorable terms. You don’t need a down payment and the loan does not come with private mortgage insurance. Movement doesn’t charge lender fees for VA loans. You’ll need a credit score of at least 580 for a conforming VA loan and 620 for a loan above the limit to qualify for a VA loan through Movement Mortgage.

Federal Housing Administration (FHA) loan: You can qualify for this type of government-backed loan with down payment savings (or gift funds) of just 3.5%. FHA loans help those who don’t have credit scores high enough to qualify for a conventional loan. The downside is that you have to pay upfront mortgage insurance and a monthly insurance premium if you put less than 20% down.

United States Department of Agriculture (USDA) loan: Low-to-moderate income homebuyers can benefit from this government loan option that requires no down payment. The property must be in a designated rural area to qualify.

Fannie Mae HomeReady®: This home loan is for those who lack down payment savings but have a good credit history and stable job. The HomeReady® program offers fixed-rate loans to low-to-moderate income homebuyers and down payments as low as 3%.

Reverse mortgage: Designed for individuals 62 or older who need income, home equity conversion mortgages, known as reverse mortgages are offered by Movement Mortgage. This loan turns your equity into cash.

Renovation loans: Movement Mortgage offers FHA 203(k) standard and limited renovation loans for those with a 580 credit score or higher, HomeStyle® Renovation mortgages and HomeStyle® for Investors, which in most cases requires a FICO score of 620 or above.

Refinance: You can refinance your VA loan, FHA loan or conventional loan at Movement Mortgage. Products offered include a fixed-rate conventional mortgage refinance or cash out for those with 620 credit score, the VA Interest Rate Reduction Refinancing Loan (IRRRL) and FHA 203(b) streamline refinances.

What Can You Do Online With Movement Mortgage?

While Movement Mortgage’s website looks slick and up-to-date, if you’re actually trying to find specific information - such as what loan terms are offered - it’s not so helpful. The list of possible loans, such as conventional, FHA and VA, gives you minimal information. You won’t find specific loan terms (such as 5/1 ARM or 15-year fixed-rate) and you won’t find any rates listed. There are no new homebuyer courses or articles, no frequently asked question section and no search bar. In general, it’s hard to find anything specific. You have to contact a loan officer to get answers to most questions.

If you’d like to apply for a loan, you’re prompted to watch a roughly three-minute long video. Casey Crawford, Movement’s CEO, introduces himself and asks you visit the Consumer Finance Protection Bureau and learn about the mortgage process before proceeding with an application. He stresses the importance of finding out how much house you can afford before applying for a loan, and says, “We want to make sure the house of your dream fits in your real-life budget.”

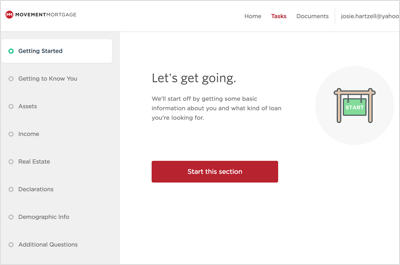

Under the video is the button to proceed to the application. There, you create an account on the Movement Mortgage “EasyApp.” The online app, powered by an outside digital platform called Blend, allows you to input personal information and upload documents. You can finish the entire mortgage application using this online platform. EasyApp is also optimized for mobile. That means you don’t need to download a special app to access your account. You use the same website address and can navigate the platform on your smartphone.

While you can apply online, there isn’t a prequalification or preapproval option. You have to do the whole thing or nothing at all. But, Movement Mortgage does advertise that the whole application process takes 30 minutes or less, which is the same time that some preapproval applications take.

Would You Qualify for a Mortgage From Movement?

The easiest financial marker to look at for mortgage qualification is your FICO credit score. Movement Mortgage will pull your credit score when you apply for a loan and it’s one of the main qualification considerations. While these are generally not completely set in stone, in general, Movement requires at least a 580 for a VA loan and a 620 for a HomeStyle® renovation loan.

For the rest of the loan offerings, such as conventional, jumbo and FHA, it’ll depend on your financial situation. The general rule of thumb for conventional loans is that 740 or higher will give you the most favorable loan terms. FHA loans can generally accept credit scores around 580.

Along with credit score, your debt-to-income ratio (DTI) is an important financial gauge. Your DTI is expressed as a percentage indicating your monthly debts to your monthly income. To calculate your DTI, add all your monthly debt payments (car loan, student loans, alimony, child support, credit card, etc.) and your projected monthly mortgage payment. Divide by your pre-tax monthly income and multiply by 100 for your percentage.

The lower your DTI the more likely you’ll qualify for a home loan and decent terms. A high DTI indicates your budget doesn’t have much wiggle room which can mean a higher risk of loan default or missed payments.

Down payment savings are another important factor in qualifying for a home loan. While you don’t need any for a VA or USDA loan, FHA loans require at least 3.5% and the Fannie Mae requires 3%. Conventional loans require 20% to avoid private mortgage insurance (PMI) payments. The higher your down payment, the more equity you have in the home. You’re also more likely to qualify for advantageous loan terms when you have a 20% down payment.

What’s the Process for Getting a Mortgage With Movement Mortgage?

To start, you can find a loan officer in your area using Movement’s website. Call or email to initiate the mortgage conversation. If you want to jump straight to applying for a loan, you can sign up for an account on Movement’s EasyApp and fill out all the necessary information.

You’ll need to provide information such as:

- Contact info, Social Security number, date of birth

- Purchase price

- Down payment

- Loan amount

- Asset information

- Income information

- Veteran status

After filling out these questions (which are more like prequalification questions), a loan officer will contact you to discuss what type of loans you might consider. If you continue on with Movement Mortgage, you’ll need to provide documentation of the information you provided. Movement asks that borrowers provide financial documents as fast as possible to get your loan moving. In general, you need to provide:

- Tax returns for the past two years

- Current pay stub and two years of W-2s

- Personal bank statements

- Asset statements, including 401(k), brokerage accounts, mutual funds, etc

- Purchase agreement

- Identification (such as your driver's license)

After your lender receives all the information, your loan will be processed and then underwritten if you’re qualified. Movement Mortgage also schedules an appraisal during this time frame. After underwriting, you’re “approved with conditions.” This means any issues with your application will have to be addressed before processing. Movement Mortgage boasts a “goal-oriented” approach to processing, this means they aim to generate closing documents within seven days, and weeks ahead of the actual closing date.

After the loan is processed, it’s time for the final underwrite where the underwriter reviews the loan and ensures you met all the conditions. The final step is closing. You’ll sign paperwork and walk out with keys to your new home.

How Movement Mortgage Stacks Up

For a non-bank lender, Movement Mortgage offers a wide variety of home loan options for every demographic. Underserved homebuyers can choose from not only FHA and USDA loans, but also Fannie Mae options. Traditional borrowers have conventional and jumbo loans to choose from.

Along with an inclusive loan offering, Movement Mortgage is widely available across the U.S. The map of loan officers connects you with a name, a face and direct contact information, which is more than many lenders offer. You can pick a loan officer to call direct; you won’t be routed through a "1-800" number. The online application platform is also one of the best SmartAsset has seen among the lenders we’ve reviewed. It’s intuitive and easy to use, and offers mobile access too.

What’s lacking at Movement Mortgage is full transparency. Unlike Wells Fargo and U.S. Bank, you won’t find rate examples or a full listing of mortgage terms. Everything feels a little general on the website. You can watch a video that features the CEO or discusses the home loan process, but you can’t find a search function on the site or a comprehensive article to help first-time homebuyers navigate the mortgage process.

That said, this lender offers some of the fastest loan processing times we’ve seen, boasting a seven day turnaround for three-quarters of all loans. If you need to get a mortgage in a hurry, this may be one of your best options. However, keep in mind that government-backed home loans, or any specialized loan program such as Fannie Mae generally come with additional requirements, separate appraisal standards and take longer to process overall. The seven-day processing likely applies to conventional loans.

Tips for Finding a Mortgage

- There can seem to be an endless sea of loan options when you're mortgage hunting, but there is one thing to look for if you find two similar lenders. While interest rates are flat, annual percentage rates (APRs) include outside charges, like closing costs and other fees. So if one lender has a larger difference between their interest rates and APRs than another, you may want to choose the one with presumably lower fees.

- A financial advisor can help you choose a mortgage that fits into your financial plan. SmartAsset free tool matches you with up to three vetted financial advisors who serve your area, and you can interview your advisor matches at no cost to decide which one is right for you. If you’re ready to find an advisor who can help you achieve your financial goals, get started now.