Sebonic Overview

Sebonic is a private mortgage lending company headquartered in Charlotte, North Carolina.

It offers conventional, VA, FHA and USDA home loans as well as mortgage refinances. The company does not offer banking options or any other financial product beyond mortgages.

Founded in 2013 by the former president of Roundpoint Financial, Sebonic operates as a subsidiary of Cardinal Financial Company, a Charlotte-based mortgage lender founded in 1987.

Today's Rates

| Product | Today | Last Week | Change |

|---|---|---|---|

| 30 year fixed | 5.75% | 5.88% | -0.13 |

| 15 year fixed | 5.25% | 5.44% | -0.19 |

| 5/1 ARM | 6.06% | 6.06% | 0.00 |

| 30 yr fixed mtg refi | 7.21% | 7.13% | +0.08 |

| 15 yr fixed mtg refi | 6.59% | 6.73% | -0.14 |

| 7/1 ARM refi | 6.13% | 6.13% | 0.00 |

| 15 yr jumbo fixed mtg refi | 3.06% | 3.10% | -0.04 |

National Mortgage Rates

Regions Served by Sebonic

Does Sebonic Operate in My Area?

Sebonic is licensed to make mortgage loans in the District of Columbia and all states except Massachusetts.

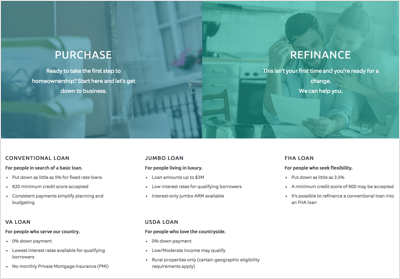

What Kind of Mortgage Can I Get With Sebonic?

Sebonic offers a number of home loan options, including:

Fixed-rate mortgage: This is the most popular type of home loan, especially for buyers who intend to stay in their new homes for a long time. The interest rate stays the same for the duration of this loan, which means that the borrower’s monthly payments also stay the same. Some may find it slightly easier to budget with a fixed-rate mortgage as you know exactly what to expect each month. Most people opt for 15-year or 30-year fixed-rate loans. With the 15-year option your monthly payments will be higher as you are paying off the same amount of money in half the time, but you will pay far less in interest over the life of the loan as compared to the 30-year option. Sebonic requires a 620 FICO credit score for a conventional loan. However, you can get a fixed-rate mortgage with an FHA loan or VA loan as well.

Adjustable-rate mortgage (ARM): Buyers who plan to move again in a few years may want to consider this mortgage option. Typically the interest rate on an ARM is lower for a fixed, initial period of one, three, five, seven or 10 years. Once that period ends, the rate adjusts and can go up or down (meaning your monthly payments will increase or decrease, as well). The loan’s terms will specify how many times the interest rate can change and also the highest possible level that it can reach. Conventional mortgage borrowers will need a 620 credit score to qualify with Sebonic.

Federal Housing Administration (FHA) loan: This is a loan that is insured by the government. Compared to a conventional loan, FHA loans have more flexible lending requirements meaning the interest rates can also be higher. This loan may be an option for you if you have a lower credit score or less money saved for a down payment. FHA loans are available as fixed-rate or adjustable-rate mortgages. Sebonic requires at least a 600 credit score to qualify.

VA loans: VA loans are mortgages that are backed by the Department of Veterans Affairs and come with benefits like low or no down payments required, no mortgage insurance premiums required and an easier approval process. VA loans are only available to current or former members of the U.S. Armed Forces, reserves and National Guard, or their spouses.

Jumbo loan: In most of the United States, the conforming loan limit is $726,200. If you get a home loan that is greater than that amount you will have a jumbo loan. In some counties where the real estate prices are higher, the conforming loan limit may be as high as $1,089,300 meaning you have a bit more room to take out a larger mortgage before it’s considered a jumbo loan. Jumbo loans are available for fixed-rate or adjustable-rate mortgages. They are considered riskier for the lender as more money is on the line if a buyer were to default on the loan. As a result, jumbo loans typically have higher interest rates. If you have a higher credit score and can afford a larger down payment, a jumbo loan may be an option for you to consider. Sebonic offers jumbo loans of up to $3 million.

USDA loan: Sebonic is an authorized lender for USDA loans, which incentivize the purchase of rural properties. If you’re interested in a property that meets USDA’s geographic eligibility requirements and you meet the income requirements, you may be able to finance a home purchase with Sebonic and put as little as 0% down.

Refinance: Existing mortgage loan holders can apply for a refinance through Sebonic. Options generally include VA loan refinances, FHA refinances and conventional mortgage refinances. If you choose to refinance, you may qualify for a lower rate or more favorable term, but you’ll have to pay closing costs on the loan again.

What Can You Do Online With Sebonic?

Sebonic has a minimal website. Loan terms and interest rate information isn’t offered online and explanations for each loan type offered are just a few sentences. You won’t find first-time homebuyer education materials, videos or a blog or article list like you’ll find on many other mortgage lender websites. There is a calculator, but that’s it on the borrower mortgage tool front.

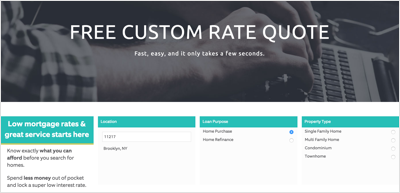

You can’t prequalify online, but you can submit information about your credit score, target home price and the location where you want to purchase property with the rate quote option. Once you’ve entered this information and your contact details, a representative from Sebonic will get in touch with you. That means you won’t find an instant answer on Sebonic’s site, you’ll have to wait to find out your quote.

On the plus side, Sebonic offers eSign and real-time status updates so you can track your loan’s progress once you’ve moved on to the application step. You can drag and drop required documents and add your signature without having to sign and scan, or sign and fax the paperwork.

The company does not have a mobile app, but the website is responsive. The text changes sizes to fit your phone and the site is optimized for the mobile experience.

Would You Qualify for a Mortgage From Sebonic?

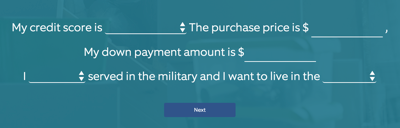

Most mortgage lenders look to your credit score as the initial qualifying factor. Sebonic accepts a score as low as 600 for an FHA loan. Conventional loans require at least a 620 FICO score. Your other loan options, including VA, USDA and jumbo, have no specified minimum score. But, to get the best rates, most lenders recommend a 740 or better credit score.

Another consideration is your debt-to-income ratio, or DTI. This figure, expressed as a percentage, helps the lender understand how mortgage payments will fit into your budget. In general, you want to keep your DTI to 36% or less. However, FHA, USDA and VA loans may tolerate a higher percentage; it depends on the lender. To find your DTI, add your monthly debt obligations together, including your car payment, student loans, credit card bills, alimony or child support. Add your projected monthly mortgage payment to this number and divide by your monthly pre-tax income. Finally, multiple by 100 and you’ll have your DTI.

Lenders also want to know how much of a down payment you’ll make when they consider you for a home loan. Sebonic allows you to put as little as 5% down for a conventional, fixed-rate loan. FHA loans require as little as 3.5% and USDA and VA loans have no down payment requirement. While you may not have down payment savings, you do still need some savings so that the lender knows you can cover closing costs and at least a few months of your mortgage payments.

What’s the Process for Getting a Mortgage With Sebonic?

You can start with a free rate quote from Sebonic’s website. Enter information such as your your zip code, loan purpose (purchase or refinance), property type, credit score and income and employment details. To get the quote, you’ll need to enter your email and phone number. After you’ve submitted the request, you’ll receive a phone call or email from a Sebonic representative who will talk to you about your mortgage options.

Once you’re ready to apply for the loan, you can call or email the company to gain access to the company’s online application platform. Sebonic boasts “drag-and-drop document capability, eSign and real-time status updates for maximum convenience and transparency,” which is typical for most web-savvy mortgage lenders. You’ll use the system to input your personal information, upload financial documents such as your W-2, tax returns, pay stubs, bank account statements, asset documentation and any further paperwork requested by your loan officer.

Sebonic doesn’t give an exact timeline of how long it will take for your loan to process. But, it does brag that Octane, its proprietary technology, speeds up the process considerably.

Once your loan is processed, the next step is underwriting. All final documents will be signed and completed, and you’ll close on the home.

How Sebonic Stacks Up

To some extent, your experience with Sebonic will depend on the quality of your interaction with the loan representative you speak to on the phone. You can’t prequalify online or start a mortgage application without getting in touch with a representative, so if you’re looking for a seamless online experience, you should look elsewhere. Rocket Mortgage, Ally, Lenda and Better Mortgage are all options for digital-savvy home lending.

Sebonic also doesn’t offer the transparency you’ll find with other lenders. You won’t see rate tables, homebuyer education or any of the tools easily found on competitor websites. That said, the company does offer the big three government-backed home loan options: VA, FHA and USDA which is something you won’t find with all non-bank lenders, like Better Mortgage.

When it comes down to choosing what company to work with, consider what interests you most. Looking for the best rates? You’ll have to call multiple companies and shop around. If you want all your financials in one spot, you could consider Wells Fargo, Bank of America or another large institution that offers home loans along with retail banking. However, if you’re hoping to complete everything online with minimal to no phone or in-person interaction from prequalification to application, you have a large number of options. Sebonic is somewhere in-between. It’s a non-bank lender that offers a wide range of loan options, but lacks transparency about rates and loan offerings and doesn’t quite offer the full online experience yet.

Tips for Finding a Mortgage

- There can seem to be an endless sea of loan options when you're mortgage hunting, but there is one thing to look for if you find two similar lenders. While interest rates are flat, annual percentage rates (APRs) include outside charges, like closing costs and other fees. So if one lender has a larger difference between their interest rates and APRs than another, you may want to choose the one with presumably lower fees.

- A financial advisor can help you choose a mortgage that fits into your financial plan. SmartAsset free tool matches you with up to three vetted financial advisors who serve your area, and you can interview your advisor matches at no cost to decide which one is right for you. If you’re ready to find an advisor who can help you achieve your financial goals, get started now.